How Christian Parents Can Blend Faith and Finances

How Christian Parents Can Blend Faith and Finances

A fast-paced life of work and family leaves parents with very little time to spare, making it easy to overlook life essentials like faith and financial management. With a bit of well-directed guidance, can you bring these parts of your life together?

As a Christian, you are faced with two essential questions concerning the uses of your money. First, are you doing what God wants with the financial resources He has given you? Second, are you using strategies that are biblically responsible? If you have a basic understanding of what the biblically responsible money issues are, you can better decide what matters to you. The use of money today is driven by financial products. Understanding how to recognize biblically responsible use of money will help you decide which financial products you want to use.

Start your re-focusing of faith and finances by looking at an overview of the common money challenges that most families face. An overview will help you see how other families that are similar to your family are managing their money. A general assessment will also help you identify goals for your family and help you stay faithful to your religion.

A Financial Overview of Marriage and Children

When you decide to marry and have children, your life goes something like this. First, there are you and your spouse, who become one through marriage. If you decide to have children, by the grace of God, you either conceive or adopt. You parent your children to adulthood at which point they go to lead their own life. From birth through age 17, lower income families in the United States can expect to spend about $174,690 to raise a child. Middle-income families can expect to pay about $233,610, and upper-income families can expect to spend about $372,210 for each child from birth through age 17 (USDA, 2017).

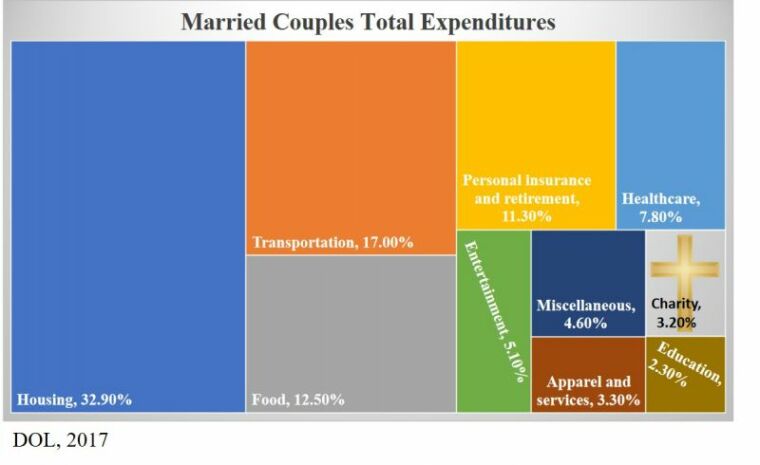

If you are a current or future parent, do not be shocked by these numbers. Most people do not realize what their future expenses are going to be, so by learning what is ahead, you know more than most parents. Understanding that you are going to have sizable future costs should help you realize that you need to know how to make the most of what you do have. The following treemap graph shows how the average married couple with children spends their money. How do you compare to this average family?

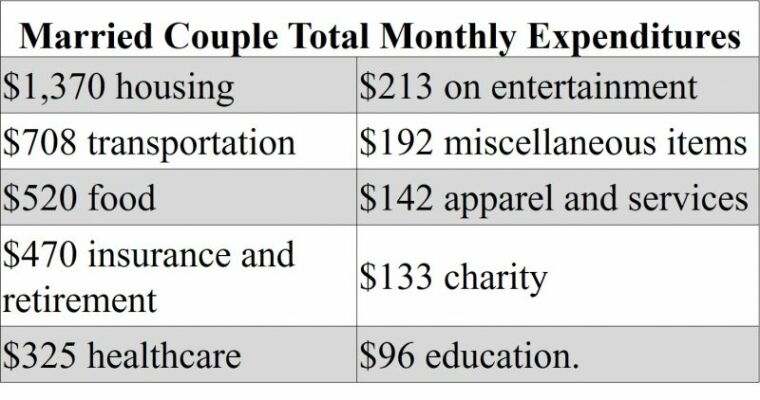

Here is a different way to look at this same information. If you clear about $50,000 per year, after taxes, and use the percentages from the previous treemap graph, the information below will show you what this would be in monthly expenditures.

If this example represented your life, what would you change? Being methodical and thinking through how you spend money is extremely helpful. In all of your planning, remember to ask God for the guidance and wisdom to help you make the best decisions on how to allocate the gifts that He has given to you.

Two great smartphone and desktop apps will help you budget your money. The first app is Mint, a free app. However, it does have some limitations. For example, you may not be able to keep track of some of your bills in their system because they do not have an agreement with certain companies. Mint does heavily promote the use of their partner companies. It is a free service and guides users to certain vendors is a way where Mint makes profits. Another budgeting app is You Need a Budget or YNAB. This app costs $6.99 per month. However it is well worth the cost. YNAB has free online classes that will teach you budgeting and personal finance.

How Families Spend Their Money.

You can summarize how you spend your money with five broad categories: giving, living expenses, debt repayment, taxes, and savings. Using Mint or YNAB will help you keep track of these five critical items. For Christians, knowing how much you can give to your Church is very important. While the New Testament of the Bible does not provide a specific percent that Christians should give to their Church, there is other guidance. Paul the Apostle preached to the Christians in Corinth, "You must each decide in your heart how much to give. And don't give reluctantly or in response to pressure. For God loves a person who gives cheerfully" (2 Corinthians 9:7, NLT). God does not want you to try harder to make more money. He wants you to trust Him. If you stop trying harder and start trusting God, this will change everything in you.

When you get to the point that you know how you are spending your money, you are ready to learn how to spend money more wisely. Plus, knowing where your money is going will help you to be aware of the biblically responsible aspects of your finances. The biblically responsible use of money is focused on what Christians may want to avoid. You may want to avoid anti-Christian organizations or non-Christian causes. There are nine major areas that most Christians consider:

- Tobacco

- Abortion

- Pornography

- Non-Christian Entertainment

- Non-Christian Lifestyles

- Alcohol

- Gambling and Gaming

- Corporate Governance

- Environmental Negligence

Almost all Christians agree that some of these issues are not biblically responsible and they have no problem avoiding the products or services of companies that engage or support these issues. Then there are some of these issues that some Christians believe do not pose a threat to their faith or Christian causes. The goal is to feel confident that you are fulfilling your duty to God as it relates to planning your family's financial well-being.

Insurance and investments are central to most people's finances. How to handle dealing with businesses in these categories is a question for each individual or married couple. This reference is not a suggestion to compromise your religious principles. Consider how scripture would apply. Suppose that twenty years ago, you purchased a life insurance policy to protect your family in the event that you die. Now the life insurance company donates money to a non-Christian group. You cannot qualify for different life insurance because your health has declined. Do you drop the life insurance and go without, or do you keep the life insurance policy? Do you believe that as a Christian consumer, you should only deal with businesses that are 100% biblically responsible 100% of the time? Consider how Bible scriptures would apply.

Paul the Apostle wrote a great deal about how to relate to the non-Christian world. Recall that Paul lived in a time when there were few Christians. They were often ridiculed and persecuted. In Paul's letters to the Christians in Colossae, he said, "Live wisely among those who are not believers, and make the most of every opportunity. Let your conversation be gracious and attractive so that you will have the right response for everyone" (Colossians 4:5-6, NLT). In Paul's letter to the Christians in Ephesus, he wrote, "so be careful how you live. Don't live like fools, but like those who are wise. Make the most of every opportunity in these evil days. Don't act thoughtlessly, but understand what the Lord wants you to do (Ephesians 5:15-17, NLT). Paul was in prison in Rome when he wrote both letters, and Paul was still encouraging Christians to be tolerant with non-believers.

Publicly traded companies that you buy for investment purposes are easier to replace if you find you don't agree with their adherence to biblically responsible morality. If you do not feel qualified to research this yourself, several investment portfolios do adhere to biblically responsible investing. You can also consult with a financial advisor. A few popular examples of groups that can help are Inspire Investing, The Timothy Plan, Guidestone Funds, Eventide, and Ava Maria Funds. All these companies offer managed portfolios that follow biblically responsible principles. Read the basis of each fund group's investment philosophy and see how they approach investing in the nine previously mentioned non-Christian causes. You will find some differences.

Doing business with life insurance companies from a biblically responsible perspective is unique. When a consumer purchases life insurance protection they expect it to usually last many years. If the life insurance company culture changes, it may be difficult if not impossible to find a substitute for that company's services.

There are two types of companies that offer life insurance protection; life insurance companies and fraternal organizations. There is a significant difference between the two. Life insurance companies are licensed in each state that they do business. They must maintain certain levels of liquid investment reserves to back up the life insurance benefit guarantees that their companies provide to their customers. A result of each life insurance company's adherence to individual state's reserve and legal requirements is that some states give the consumers some assurances that their life insurance protection will be guaranteed.

Fraternal benefit societies are operated differently. The business concept of fraternal organizations that offer life insurance is to be a service provided to members of each respective organization. For example, the largest fraternal benefit society is Thrivent Financial for Lutherans which operates for Christians. Any Christian may join their society and purchase life protection through their organization. It is important to notice that fraternal benefit societies do not sell life insurance policies. Members receive a life insurance certificate. The difference between a policy and a certificate is how the individual states regulate life insurance companies and fraternal benefit societies.

Life insurance companies have a much higher investment reserve requirement. Fraternal benefit societies have lower reserve requirements. Additionally, life insurance company customers have a higher level of state oversite and protections available as opposed to the fraternal benefit societies. That means that smaller fraternal benefit societies can operate with lower capital requirements which could put more financial risk upon members if the fraternal benefit society cannot back its guarantees.

A misconception among fraternal benefit society members is that the organizations only invest their assets in biblically responsible investments. Recently, Advice4LifeInsurance.com surveyed approximately sixty of the largest fraternal benefit societies and asked if they screened their investments for the nine non-Christian causes previously mentioned. The overwhelming majority of fraternal benefit societies declined to participate in the survey. "Thrivent takes the position that they have a fiduciary responsibility (to consumers) that supersedes its ability to screen for moral ethical or biblical purposes (Short, 2010).

The same survey was sent to many large life insurance companies, and the sentiment was the same as the fraternal benefit societies, they declined to participate. Without a response, you have to form your conclusions. One theory is that life insurance companies and fraternal benefit societies may refuse to offer an opinion because they do not want to offend consumers. If they take a stance on the biblical responsibility of their investments and their screening does not match consumers, then they run the risk of offending Christians and non-Christians. So, what are Christian consumers to do about life insurance?

If you are a member of a fraternal organization, your inquiry into the biblically responsible investment screening process of that organization may be answered quicker than someone from the outside. Have a list of the nine non-Christian causes and ask if your fraternal benefit society screens for any of those causes. If enough of the fraternal organization's members inquire, it can shape the policies of the fraternal benefit society.

A similar occurrence has happened with investments. More and more consumers have shown an interest in investments that are socially responsible. Investment companies that screen for biblically responsible investments are similar to investment companies that screen for socially responsible investments. The general public's opinion on environmental and climate change issues has prompted the creation of more socially responsible investments. More and more people have become concerned about human trafficking and other human rights as well. An increase in some consumers' awareness to some of these social issues has led them to seek investments that are socially responsible.

The same type of occurrence has happened with biblically responsible investments. A growing number of Christians have shown concern with the moral and ethical attitudes of the publicly traded companies in which they invest. As a result, more companies are being created to cater to Christians interested in biblically responsible investments. If more Christian consumers show concern over the biblical responsibility of insurance companies or fraternal benefit societies, they will begin to screen out investments that are involved in non-Christian causes.

Some life insurance companies do screen for non-socially responsible causes. An insurer that is at the forefront of socially responsible investing within the insurance industry is John Hancock Life Insurance Company. John Hancock Life Insurance Company is a US company that is a subsidiary of Manulife, a Canadian life insurance company. Manulife/John Hancock states that "From climate change to corporate board diversity, environmental, social and governance (ESG) issues are more important than ever in today's business environment." The company goes further to outline their initiative by stating that they will not knowingly invest in companies that are involved in any of the following: gambling, tobacco, alcohol, weapons, adult entertainment or nuclear energy (Manulife/John Hancock, 2017). You can see that the areas are similar to biblically responsible investing with a few notable differences: abortion and non-Christian lifestyles. Further research of Manulife/John Hancock does not indicate that they have supported any organizations involved in abortion.

If you have a life insurance policy through a company that is not conducting business the way that you live your life, consider how it is related to your life. Big businesses are not real people. People in businesses change, and that does not change who you are. As Paul said, "Live wisely among those who are not believers" (Colossians 4:5, NLT).

We live in a complicated society and just as Paul the Apostle stated, we are to "make the most of every opportunity in these evil days" (Ephesians 5:16, NLT). That does not mean to be nefarious in your actions. It does mean that you should not let the actions of non-believers force you to put your family's future at risk. Go to God in prayer and ask for guidance in making your financial plans. With His guidance, make plans that are sufficiently specific enough to be meaningful, yet flexible enough to be practical for changes that may occur within the economy and within your family.

– Van Richards is a Christian financial advisor as well as the founder of https://www.Advice4LifeInsurance.com and http://www.Advice4Retirement.com. Van draws from his 30 years as a financial advisor to write about financial issues from a Christian perspective. You can contact him at van@advice4lifeinsurance.com.